8. What is the Discounted Cash Flow (DCF) Model?

The Discounted Cash Flow (DCF) model is one of the most fundamental and widely used methods in company valuation. It is grounded in a simple but powerful idea:

The value of a business today is equal to the total amount of cash it will generate in the future, brought back to the present using a discount rate that reflects the time value of money and investment risk.

Rather than relying on current stock prices or market trends, the DCF model focuses on the intrinsic value of a company based on its expected future financial performance.

Why DCF Matters to Investors

- Helps assess whether a stock is overvalued, undervalued, or fairly priced

- Especially useful for long-term investors, analysts, and fund managers

- Shifts the focus from short-term market sentiment to long-term cash flow potential

Core Principle: Time Value of Money (TVM)

The time value of money suggests that ₹100 today is worth more than ₹100 a year from now, due to its potential to earn returns.

The DCF model uses this principle to convert future cash flows into present value using a discount rate (usually the company’s Weighted Average Cost of Capital (WACC) or a required return rate).

Key Components of a DCF Model

1. Free Cash Flows (FCF)

Free Cash Flow represents the cash available to the business after accounting for capital expenditures needed to maintain or grow operations.

Formula:

These are projected for a period (usually 5–10 years).

2. Discount Rate (r)

This reflects the risk associated with the business and the investor’s required return.

- High-risk businesses → higher discount rate

- Stable businesses → lower discount rate

For DCF, the WACC (Weighted Average Cost of Capital) is commonly used, as it blends the cost of equity and debt.

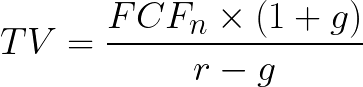

3. Terminal Value (TV)

Since it's hard to forecast cash flows indefinitely, a terminal value accounts for the cash flows beyond the explicit forecast period.

It is typically estimated using:

- Gordon Growth Model (Perpetuity Method):

- or the Exit Multiple Method.

4. Present Value (PV)

Each year’s cash flow and the terminal value are discounted back to the present using the discount rate.

DCF Formula (Simplefied)

Sample Illustration (Conceptual)

Assumptions:

- Free Cash Flow for next 5 years = ₹100 crores/year

- Discount rate = 10%

- Terminal value at end of Year 5 = ₹600 crores

| Year | Cash Flow (₹ Cr) | Discounted Value |

|---|---|---|

Total DCF Value = ₹751.61 crores

If the market cap of the company is ₹650 crores, it is potentially undervalued.

Advantages of the DCF Model

- Focuses on actual business performance, not market speculation

- Especially effective for cash-generating businesses

- Provides a theoretically sound, forward-looking estimate of value

- Useful for investment decision-making, mergers, acquisitions, and capital budgeting

Limitations and Risks

- Highly sensitive to assumptions (small changes in discount rate or growth rate can alter value significantly)

- Relies heavily on the accuracy of projections (difficult for startups or cyclical industries)

- Requires strong finance and accounting knowledge to apply correctly

Therefore, the DCF model should ideally be used alongside other valuation methods such as P/E ratio, P/B ratio, or comparative company analysis.

When Is DCF Most Useful?

- For stable businesses with predictable cash flows (e.g., FMCG, utilities)

- For valuing projects, investments, or entire businesses

- In long-term investment decisions, especially when price deviates from intrinsic value

Key Takeaways

- DCF is a valuation method based on future cash flow projections.

- It adjusts these cash flows to present value using a discount rate, reflecting risk.

- Helps estimate the intrinsic value of a business or investment.

- Effective but sensitive to assumptions — best used for companies with reliable financial histories.

- Supports rational investing by focusing on fundamentals, not hype.